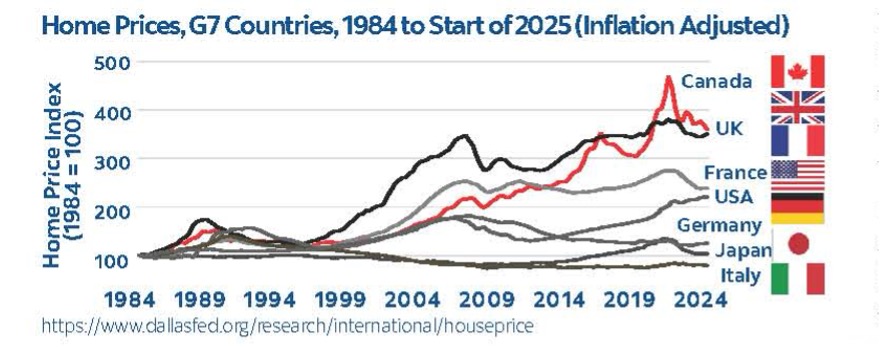

Spring marks the start of the home-buying season. While price growth has slowed, and even reversed in some markets, Canadian home prices have risen faster than those in any other G7 country (Group of Seven advanced economies), nearly quadrupling over 40 years. As a result, many view Canadian real estate as one of the best-performing long-term asset classes.

While housing has delivered attractive returns, an interesting comparison emerges since the start of the millennium: Despite a more volatile return path, the S&P/TSX Composite has generated higher annualized total returns than many real estate markets. The chart (bottom) shows performance through the start of 2025, as real estate prices moderated in major markets, in part due to higher interest rates.

Without a doubt, various factors make a direct comparison between real estate and stocks difficult. Investing in real estate comes with various challenges, including limited liquidity, significant capital outlay (partially offset through leverage, such as a mortgage), transaction costs (commissions, legal fees and land transfer tax) and ongoing maintenance (property taxes and repairs). Stock market participation is generally more accessible in terms of initial capital, transaction costs and liquidity, while offering greater diversification. Yet, the stock market can be more volatile, making downturns difficult for many investors. Different tax treatments and risk profiles further complicate direct comparisons.

The recent moderation in housing markets serves as a reminder that even long-standing trends can shift. Yet, Canadians have been fortunate that both real estate and equities have offered substantial wealth-building opportunities over recent decades.

Sources: 1. S&P/TSX Composite Total Return Index (dividends reinvested);

2. to 7. Teranet-National Bank House Price Index, https://housepriceindex.ca/;

02/99 to 02/25, based on Bloomberg/RBC Wealth Management analysis.

Be Aware: FHSA Contribution Room May Be Incorrect

If you’ve helped a young family member open a First Home Savings Account (FHSA), be aware that the Canada Revenue Agency (CRA) may have inaccurate contribution data. The consequence? The one percent per month penalty on excess contributions, which quickly adds up. A recent Globe & Mail article highlighted the issue: “Schedule 15—FHSA Contributions, Transfers and Activities” must be attached to a tax return whenever a contribution or withdrawal is made.1 This form was introduced in 2023 and some tax software did not automatically include it, leading certain 2023 contributions to be misclassified as 2024 overcontributions. To fix this, it is advised to contact the CRA and amend the 2023 return using Schedule 15.

1. “How we fixed a $1,000 FHSA tax penalty,” B. Leung, Globe & Mail, 01/30/26, B11.

.png)